Time: ~6 min. Need: at least one month of categorised transactions in WealthSense, or your target retirement spending estimated to within €200 a month, plus your current net worth (or a guess within ten percent).

By the end of this you will have a projected year — often a month — when WealthSense thinks you can stop trading hours for money. The number changes when you change the inputs; seeing what moves it the most is where the planning happens.

FIRE planning for EU expats with US RSUs is the methodology piece. This article walks the in-app tool.

Steps

-

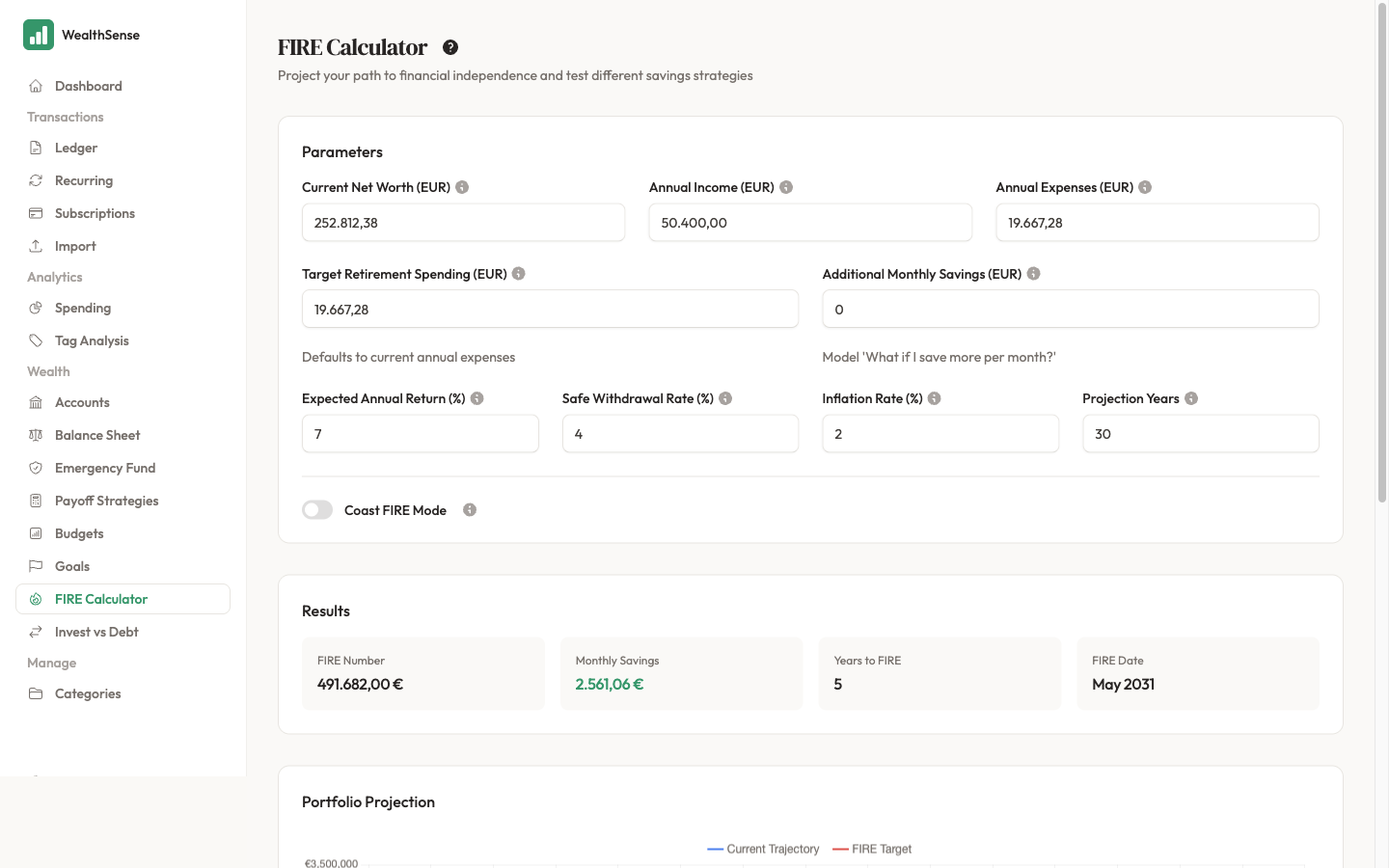

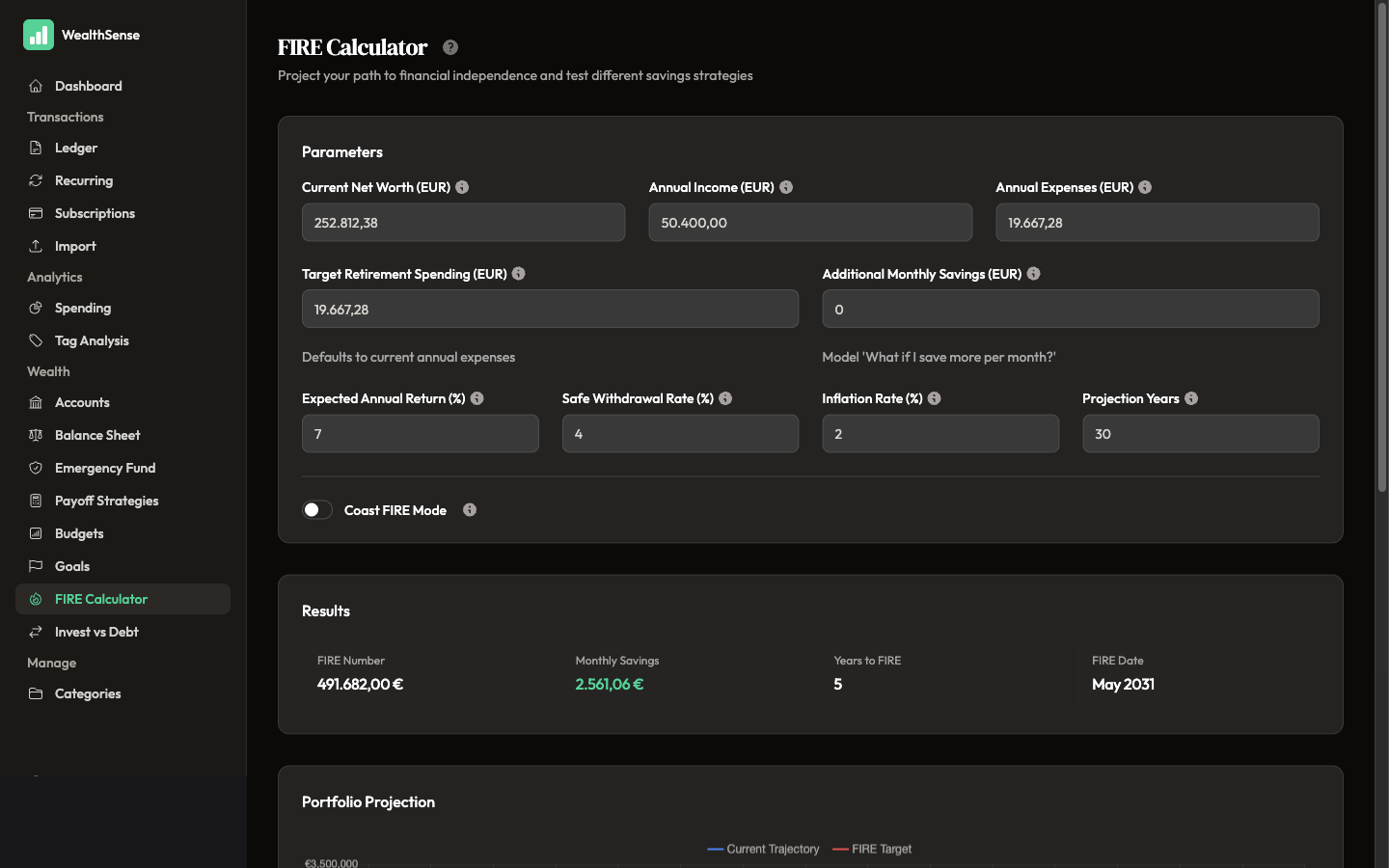

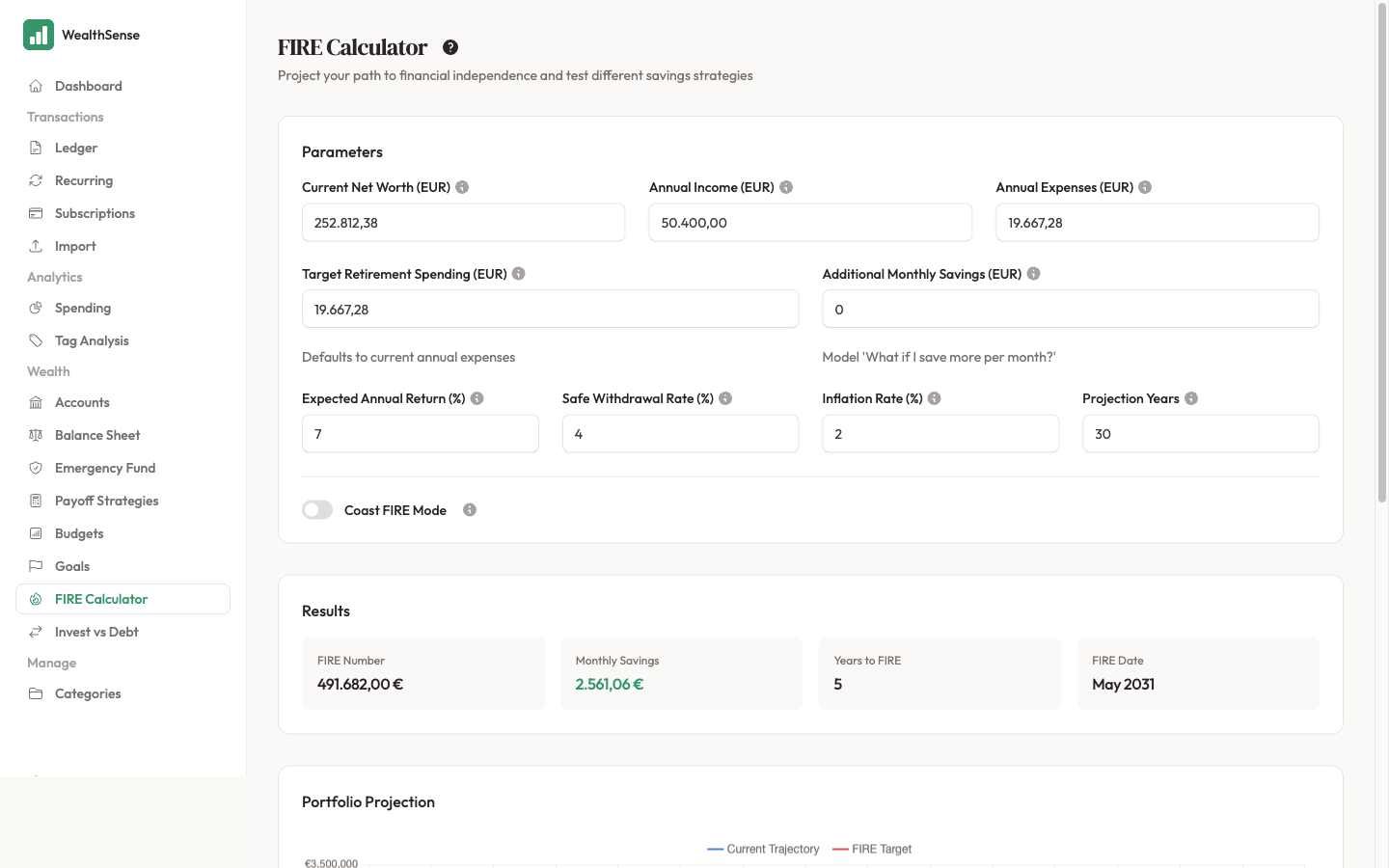

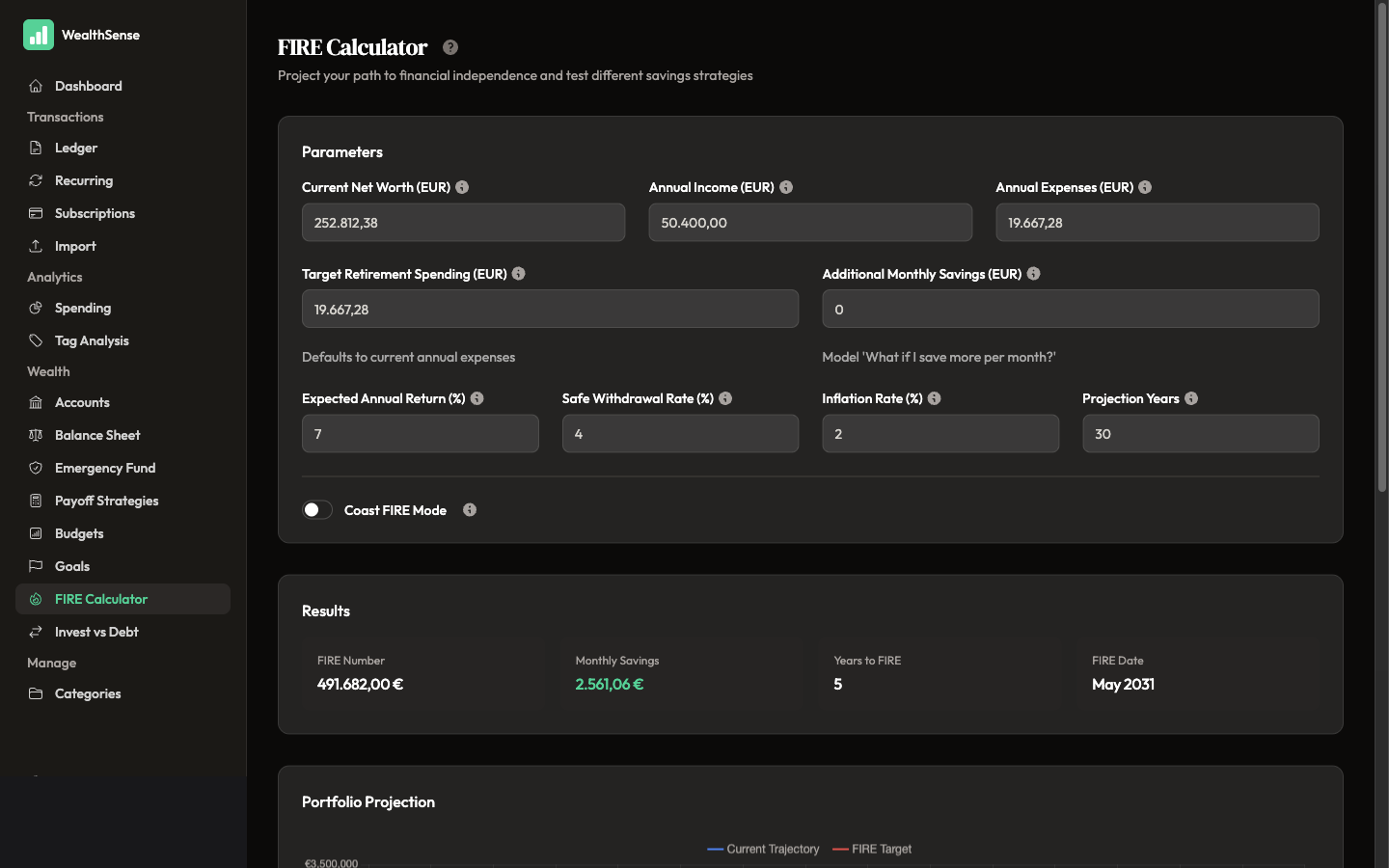

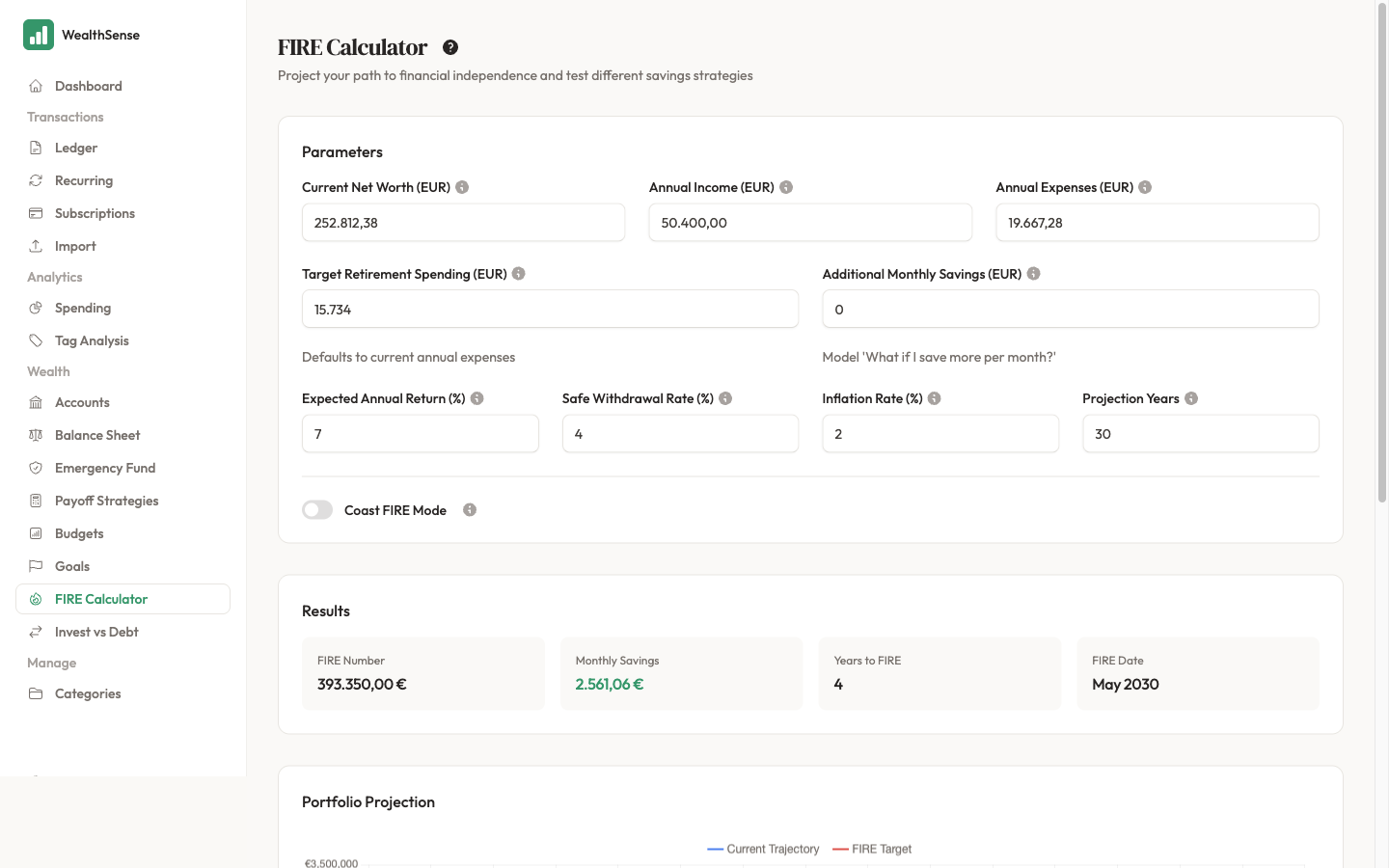

Open the FIRE calculator. From the sidebar, under Wealth, open FIRE Calculator. The page opens with your current net worth pre-filled from your accounts.

-

Confirm your Target Retirement Spending. WealthSense defaults this to your current annual expenses, then lets you override the retirement target directly. Change it if you know post-FIRE spending looks different — a baby, a sabbatical, a paid-off mortgage. The number you enter is annual post-FIRE spend, not monthly spend.

-

Pick a withdrawal rate. The default is 4% — the safe-withdrawal-rate convention from the Trinity study. Lean-FIRE readers often pick 3%. Fat-FIRE 4.5% is also defensible. Each one-percent change pushes the date by years, not months — the choice matters.

-

Read the projection. The page shows the year (and month) your accumulated net worth crosses your FIRE number — defined as your target retirement spending divided by your withdrawal rate. A separate line shows the burn-rate-down-to-zero counterfactual: how long your current net worth would last if you stopped earning today.

-

Re-run with a lean-FIRE scenario. Drop Target Retirement Spending by twenty percent and watch the date move years earlier. That is the lean-FIRE-vs-regular-FIRE trade-off in one glance: how much earlier do you reach freedom if retirement costs less?

You're done when…

You can name your projected FIRE year (or "never" if your current savings rate doesn't get you there yet), you can name two scenarios that move the date earlier, and you know which of the three assumptions — withdrawal rate, expected return, or target retirement spending — moves the date the most when you toggle it.

See also

- Stress-test the assumptions — Run scenarios on your future

- The pre-signup methodology — FIRE planning for EU expats with US RSUs

- Pay down debt vs invest — Choose a debt payoff strategy