Time: ~4 min. Need: at least one debt account in WealthSense with an interest rate and a minimum monthly payment set.

By the end of this you will have picked between two legitimate strategies — avalanche (highest interest first; lower total cost) and snowball (smallest balance first; easier psychology) — and you'll know what an extra €100 a month buys you under each.

Both strategies pay off your debt. One costs less in interest; the other gives you closed accounts to celebrate. The right pick is the one you'll actually follow for three years.

Steps

-

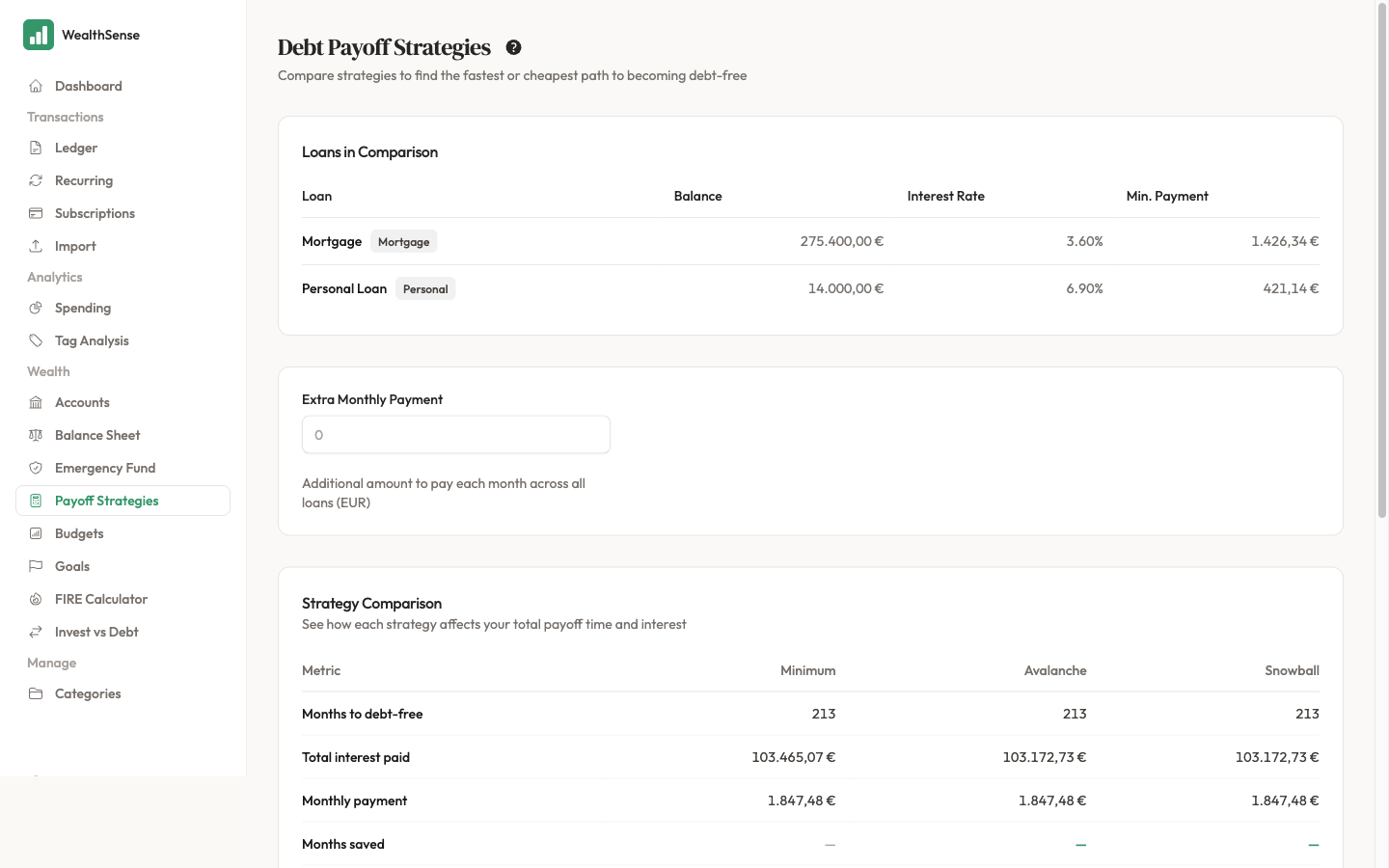

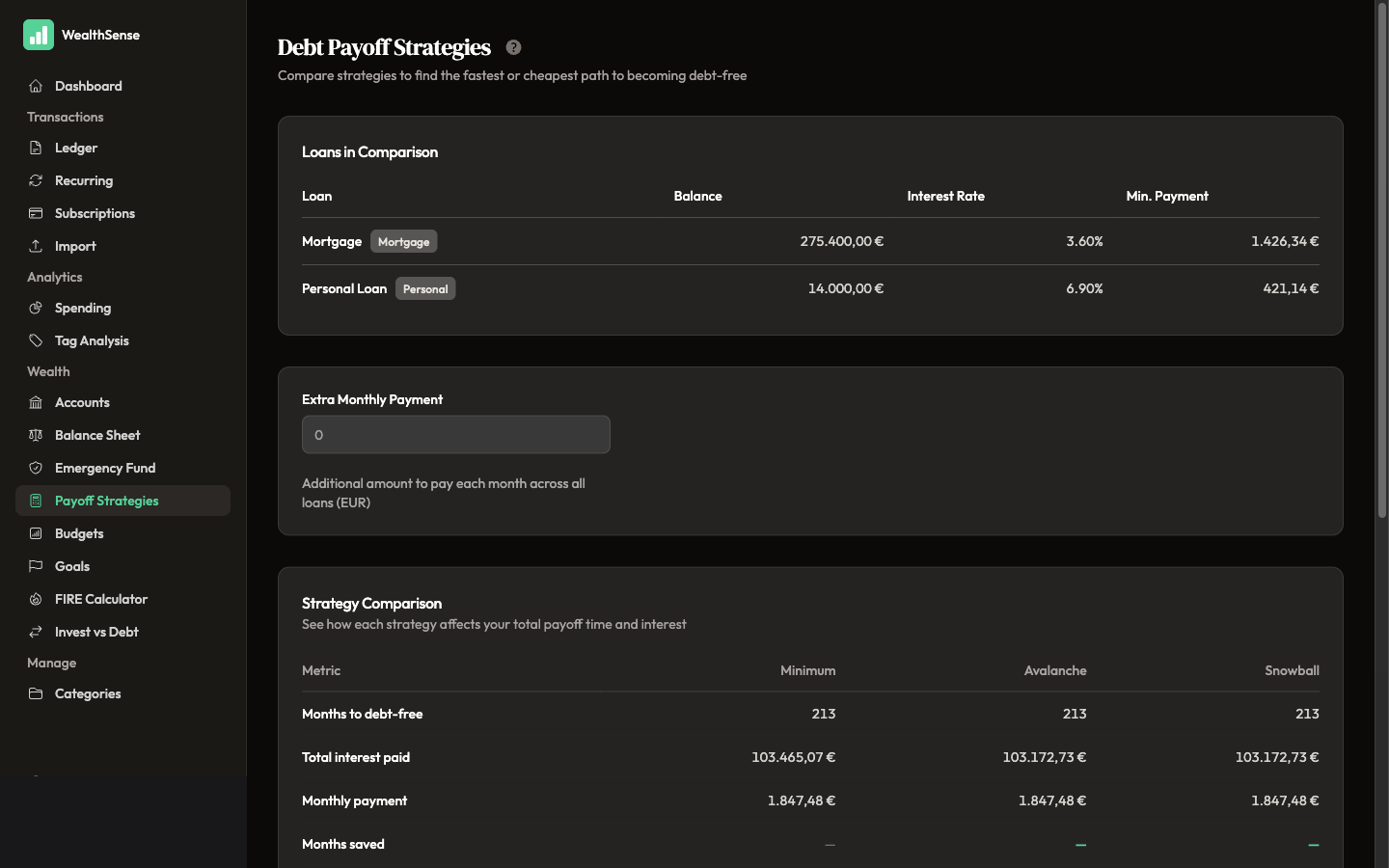

Open Payoff Strategies from the sidebar. The Debt Payoff Strategies page lists every debt account WealthSense knows about and shows the two strategies side by side.

-

Confirm every debt account is there with an accurate balance, interest rate, and minimum payment. Fix anything missing or wrong now — the projections downstream are only as good as the inputs.

-

Read the Avalanche projection: total interest, the month you become debt-free, and the order WealthSense suggests tackling each debt. Avalanche leads with the highest-APR debt and walks downward.

-

Read the Snowball projection in the next column. Same metrics, different order — smallest balance first. The total interest is higher than avalanche. The first closed account arrives earlier.

-

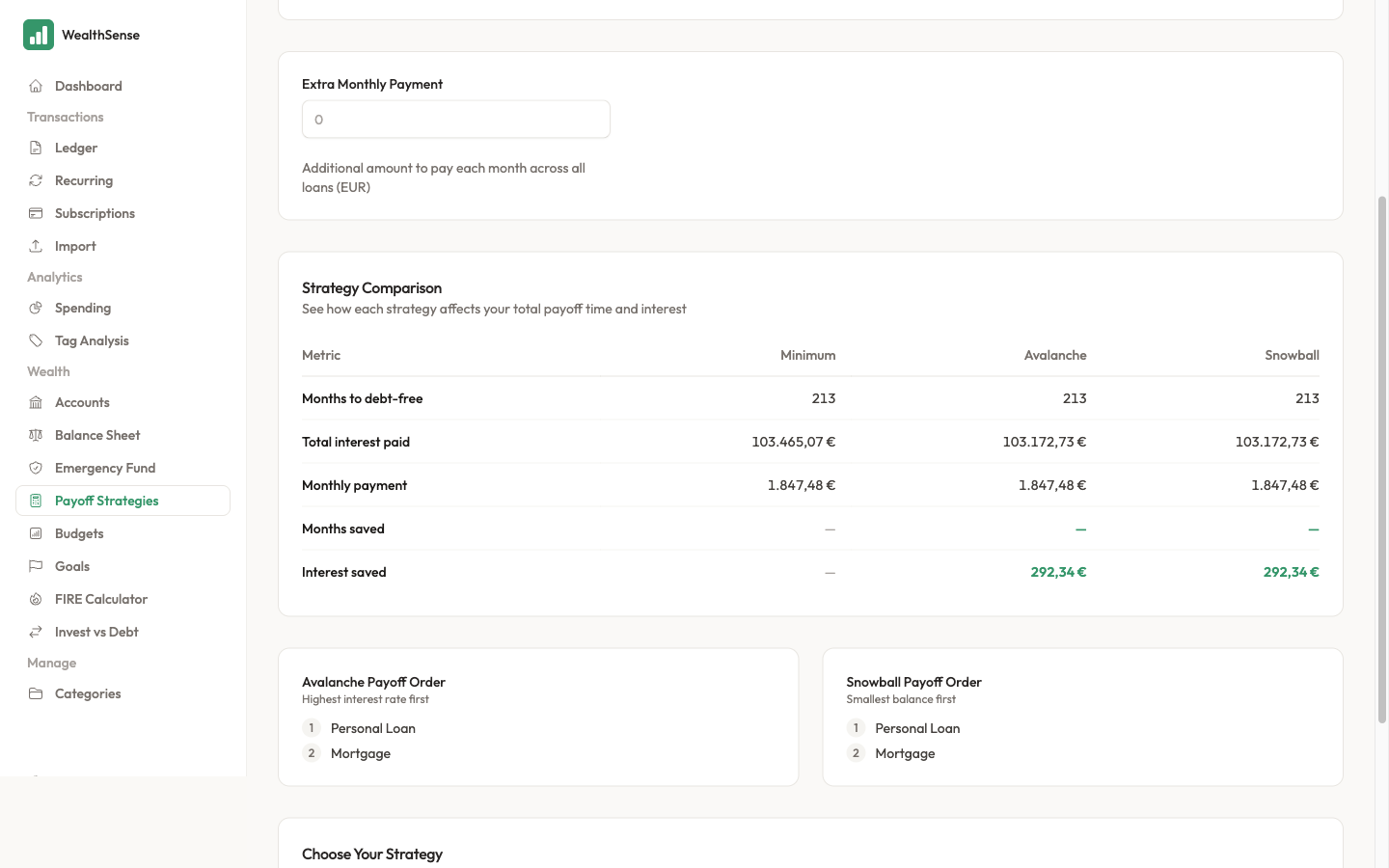

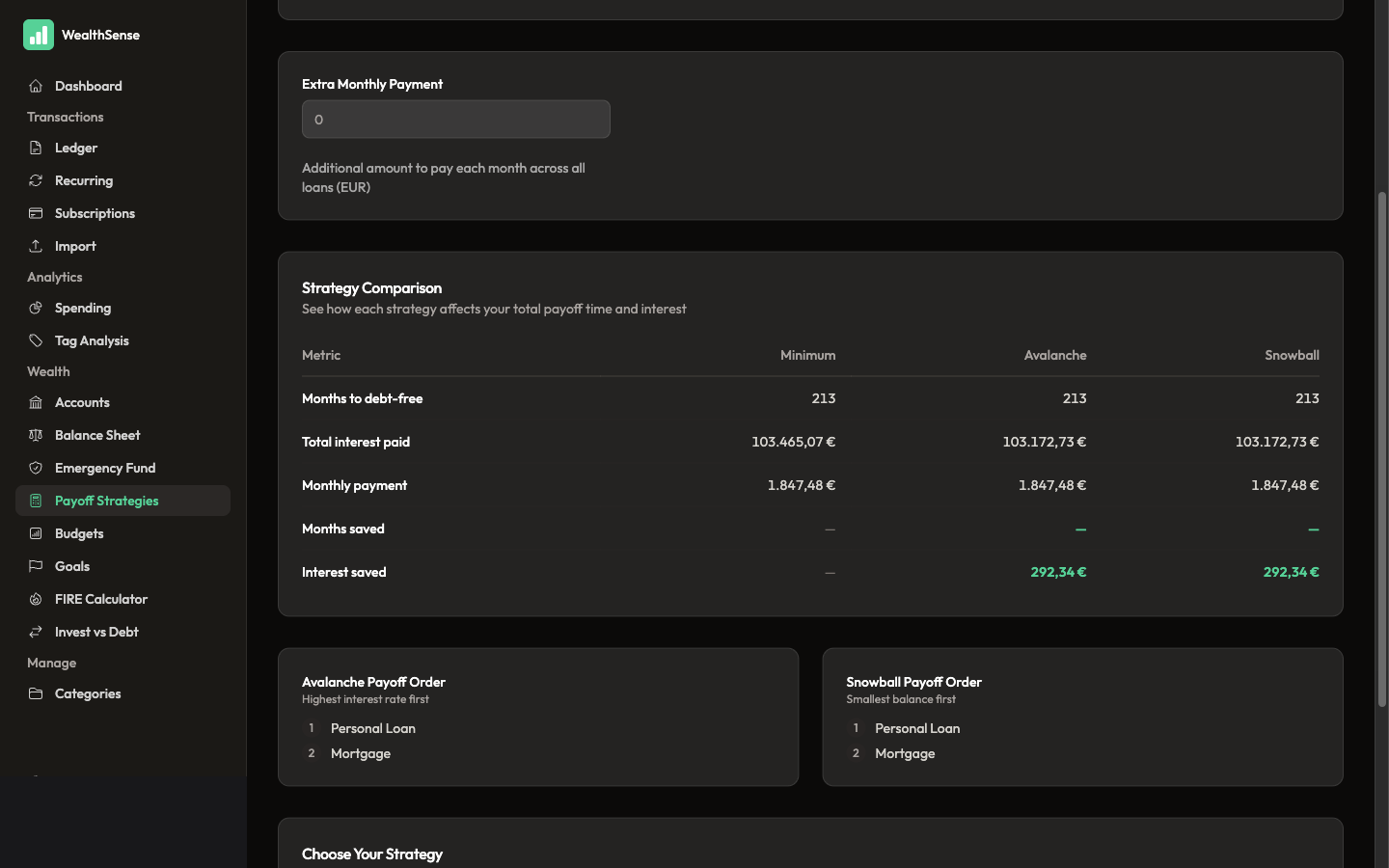

Try an extra-payment number. The slider on the comparison page lets you add an extra amount each month — try €50, €100, €250. Watch the payoff date pull in under both strategies, and watch the avalanche-vs-snowball interest gap widen or narrow. A small extra payment often saves more interest than switching strategies.

-

Pick the strategy you'll actually follow. If the interest gap is small (under a few hundred euros) and the snowball's first closed account in eight months keeps you motivated, snowball is a fine call. If the gap is thousands, avalanche pays for itself in held resolve. Both answers are right answers.

You're done when…

You know which strategy you're following, you know the total interest you'll pay under that strategy versus the other, and you have at least one extra-payment number in mind even if you can't afford it yet.

See also

- Stress-test the choice — Run scenarios on your future

- The FIRE counterpart — Plan your FIRE date

- Automate the extra payment — Set up recurring rules that match your real life